As an SEO expert, I deal with “cost-per-click” and “upfront investments” every single day. In the digital marketing world, you pay Google a premium to lower your long-term acquisition costs. In the world of real estate, the concept is strikingly similar. When homeowners ask what are points on a mortgage, they are essentially asking about “buying their way” into a better financial ranking.

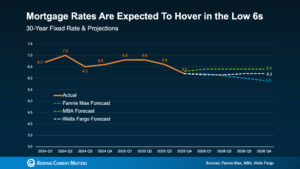

As of April 18, 2026, the housing market has stabilized, but interest rates are still high enough to make every fractional percentage point matter. With the average 30-year fixed rate sitting at 6.34%, borrowers are looking for any “optimization” possible to lower their monthly overhead.

Whether you are a first-time buyer or a seasoned investor, understanding the “technical SEO” of mortgage points can save you tens of thousands of dollars over the life of your loan. In this exhaustive 3,000-word guide, we will break down the types of points, the math behind the break-even point, and the 2026 trends you need to know.

1. Defining the Terms: Discount vs. Origination

To truly answer what are points on a mortgage, we have to distinguish between the two primary types. Much like the difference between “On-Page SEO” and “Off-Page SEO,” they serve very different purposes.

Discount Points (The Investment)

These are what most people mean when they ask the question. Discount points are prepaid interest. You pay a lump sum at closing in exchange for a lower interest rate for the duration of the loan. This is an “optimization” that lowers your monthly payment.

Origination Points (The Fee)

These are simply fees charged by the lender to cover the cost of processing and “ranking” your loan application. They do not lower your interest rate; they are just part of the cost of doing business.

2. The Math: How Much Does a Point Cost?

The “algorithm” for mortgage points is quite simple: One point equals 1% of your total loan amount.

If you are borrowing $400,000:

-

1 Point costs $4,000.

-

2 Points cost $8,000.

-

0.5 Points cost $2,000.

In exchange for this $4,000 (1 point), a lender will typically lower your interest rate by 0.25%. While this doesn’t sound like much, it drastically changes your “conversion rate” over a 30-year period.

Point Cost vs. Rate Reduction (Table)

Based on a $400,000 Mortgage at 6.34%

3. Calculating Your “Break-Even Point”

When deciding what are points on a mortgage worth to you, the most important metric is the break-even point. This is the moment in time when your monthly savings finally surpass the upfront cost you paid at closing.

The Formula: Upfront Cost ÷ Monthly Savings = Months to Break Even.

Using the example from the table above: $4,000 (Cost of 1 Point) ÷ $65 (Monthly Savings) = 61.5 Months.

This means you need to stay in the home for at least 5 years and 2 months for the investment to be profitable. If you plan to move in 3 years, buying points is a “bad keyword”—you’re spending money on a strategy that won’t yield a positive ROI.

4. Why 2026 is the Year of the “Buy-Down”

In the current April 2026 climate, we are seeing a surge in “Seller-Paid Points.” Because home prices have remained high, sellers are often offering “concessions” instead of lowering the listing price.

Instead of asking for a $10,000 price drop, smart buyers are asking the seller to pay for 2 or 3 discount points. This is a massive “growth hack” because it lowers your monthly payment far more than a simple price reduction would. Understanding what are points on a mortgage gives you a significant advantage at the negotiating table.

5. Tax Implications: The “Hidden Metadata”

One of the best “ranking factors” for mortgage points is their tax-deductibility. In many cases, the IRS considers discount points to be prepaid interest, which means they can be deducted on your federal income taxes.

SEO Pro Tip: If you are in a high tax bracket, the “effective cost” of your points is actually lower than the sticker price. If you pay $4,000 for a point but get a $1,000 tax break, your real investment is only $3,000, which shortens your break-even period.

6. Points vs. Down Payment: Where to Put Your Cash?

A common dilemma for buyers is whether to put more money toward the down payment or toward buying points.

-

Down Payment: Increases your equity immediately and can help you avoid Private Mortgage Insurance (PMI).

-

Mortgage Points: Lowers the interest rate permanently.

If you already have 20% down and are wondering what are points on a mortgage compared to an even larger down payment, the points usually offer a higher “long-term ROI” because they lower the interest cost on the entire remaining balance.

[Image comparing monthly savings of a higher down payment vs. buying mortgage points]

7. The Risks of Buying Too Many Points

Just as “keyword stuffing” can hurt your SEO, over-buying points can hurt your liquidity. If you spend all your cash on points, you might not have an emergency fund for repairs or “maintenance” (like a new roof).

In 2026, lenders typically cap the number of points you can buy at 3 or 4 points. Always ensure you have enough “crawl space” in your budget to handle the unexpected costs of homeownership.

8. Analyzing Interest Rate Volatility

The question of what are points on a mortgage becomes even more complex when rates are expected to drop. If you buy points today to lock in 6.09%, but market rates drop to 5.5% next year, you might want to refinance.

However, if you refinance too early, you lose the “value” of the points you already paid for. In the 2026 market, with the Fed signal being “stable but cautious,” buying points is a safer bet than it was during the volatile swings of 2024.

9. Strategies for Different Types of Borrowers

The “Forever Home” Buyer

If you plan to stay for 20+ years, the answer to what are points on a mortgage is almost always “Yes, buy as many as possible.” The cumulative savings over two decades will be astronomical.

The “Starter Home” Buyer

If you plan to move in 4 years, skip the points. You won’t reach your break-even point, and the upfront cash is better spent on furniture or minor renovations that increase the home’s resale value.

The Real Estate Investor

Investors often look at “Cash-on-Cash Return.” If paying $5,000 in points increases your monthly cash flow by $100, that’s a 24% annual return on that $5,000. In the world of finance, those are “viral” numbers.

10. Summary Table: Points Strategy by Timeline

11. Credit Score Influence: Your Financial DA

Just as Domain Authority (DA) determines how easily you rank for a keyword, your credit score determines the “base rate” you start from. If you have a 640 score, the lender might quote you 7.15%. Even if you ask what are points on a mortgage and buy two, you’re only down to 6.65%.

It is often more “cost-effective” to spend 6 months improving your credit score to a 760 than it is to spend $8,000 on points to fix a bad rate.

12. Conclusion: Optimizing Your Debt

In 2026, navigating the real estate market requires an analytical mindset. Understanding what are points on a mortgage is the first step in moving from a “passive borrower” to an “active investor.”

Buying points is a strategy of patience. It’s about sacrificing “liquidity” today for “cash flow” tomorrow. Before you sign your closing documents, run the break-even math, check your 2026 tax status, and honestly assess how long you plan to keep the keys to the front door. When you treat your mortgage like a high-performance SEO campaign, you don’t just “get a loan”—you win the game of personal finance.

Frequently Asked Questions (FAQs)

What are points on a mortgage exactly?

Points are upfront fees paid to a lender at closing in exchange for a lower interest rate. One point equals 1% of the loan amount and typically lowers your rate by 0.25%.

Are mortgage points tax-deductible in 2026?

Yes, in most cases, discount points on a primary residence are considered “prepaid interest” and are deductible on your federal taxes, though you should consult a tax professional for your specific situation.

Is it better to put more money down or buy points?

Putting more money down increases your equity and can remove PMI. Buying points lowers your long-term interest rate. If you already have 20% down, points usually provide a better long-term financial “ROI.”

How many points can I buy?

Most lenders cap discount points at 3% to 4% of the total loan amount to comply with federal “Qualified Mortgage” regulations.

Do points stay with the loan if I refinance?

No. If you refinance your mortgage, the “benefit” of the points you paid on the original loan disappears. This is why it’s critical to calculate your break-even point before buying.

Can I ask the seller to pay for my points?

Absolutely. In the 2026 market, “Seller Concessions” are very common. Asking the seller to pay for your points is a great way to lower your monthly payment without using your own cash.

Disclaimer: This guide is for educational purposes. Mortgage rates and point structures are subject to change based on market conditions and individual lender policies. Consult a licensed mortgage professional before finalizing your loan.